Sample 2b

.jpg "https://www.theguardian.com/") Teacher notes

Teacher notes

The following page provides you with a sample IA, graded under the new criteria and was part of the sample provided to workshop leaders, during the recent IB workshop training. Sample number 2b - macroeconomics is designed to be graded alongside sample number 2a, 2c and (FII).

Commentary 2

Title of the article: Inflation returns to Japan for the first time in more than a year

Source of the article: The Guardian

https://www.theguardian.com/world/2017/mar/03/inflation-returns-to-japan-for-the-first-time-in-more-than-a-year (Accessed 18 August 2017)

Date the article was published: 3 March 2017

Date the commentary was written: 12 October 2017

Word count of the commentary: 793 words

Unit of the syllabus to which the article relates: Macroeconomics

Key concept being used: Choice

Inflation returns to Japan for the first time in more than a year

Prices tick up helped by the rising cost of oil but a slump in household spending clouds the outlook. Japan’s core consumer prices have risen for the first time in over a year thanks to a pickup in energy costs, marking a rare victory in the government’s  long battle against deflation.

long battle against deflation.

But a slump in household spending slowed by 1.2% compared with January last year showed why economic growth and inflation have lagged the more ambitious goals set out by policymakers.

As rising protectionism in the United States poses risks for the world’s third-largest economy, as well as the rest of export-reliant Asia, there is a danger companies will shy away from boosting wages seen as crucial for durable growth.

That will also undermine the Bank of Japan’s efforts to accelerate inflation to its still-distant 2 percent target, analysts say.

Government data showed on Friday that the core consumer price index (CPI), which includes oil products but excludes volatile fresh food prices, rose 0.1% in January from a year ago, posting the first increase since December 2015.

It compared with a median market forecast for a flat growth and followed a 0.2% drop in December.

Many analysts expect core consumer prices to head toward 1% later this year helped by the strengthening US dollar pushing the yen lower. A fall in the currency will make imports more expensive for Japanese consumers, which will boost prices.

“Inflation will accelerate this year due to a rebound in energy costs and the weak-yen effect. But it won’t heighten much next year unless wages spike and boost spending ,” said Yoshiki Shinke,chief economist at Dai-ichi Life Research Institute. “The hurdle for hitting 2% inflation remains very high, which means the BOJ will maintain its ultra-loose monetary policy for the time being,” he said. Slow wage growth is weighing on consumer spending – which accounts for more than a half of Japan’s GDP – despite a tight jobs market.

Unemployment has been at its lowest level in around 20 years. Fresh data on Friday showed the jobless rate edged down from 3.1% in December to 3% in January.

This week, Japan posted an unexpected drop in factory output for January, the first fall in six months and the latest red flag for the world’s number three economy.

Japan has been struggling to reverse a years-long deflationary spiral of falling prices and lacklustre growth. “The government is teaming up with the Bank of Japan to keep working toward getting out of deflation,” top government spokesman Yoshihide Suga told reporters Friday.

Tokyo’s years-long effort to kickstart growth – a blend of massive monetary easing, government spending and red-tape slashing – stoked a stock market rally, weakened the yen and fattened corporate profits, but growth in the wider economy remains fragile.

Commentary

The Bank of Japan (BOJ), and the Japanese government are trying to stop deflation, the sustained decrease in the consumer price index (CPI). It may seem that an economy is better off choosing deflation, rather than its opposite—inflation. But deflation in Japan has been accompanied by falling and even negative growth rates of real GDP. Therefore, they have made the choice of promoting inflation, aiming for 2% per annum. In addition to the government making policy choices, firms are choosing whether or not to invest, and households have difficult choices to make about consumption and wages.

One reason why Japan has difficulty in preventing deflation is the protectionist policies that are being used by the United States to limit foreign firms’ imports. These policies make it difficult for Japanese firms to export their goods, which in turn makes firms less likely to raise their wages. Therefore, consumption spending has actually fallen by 1.2% over the last year.

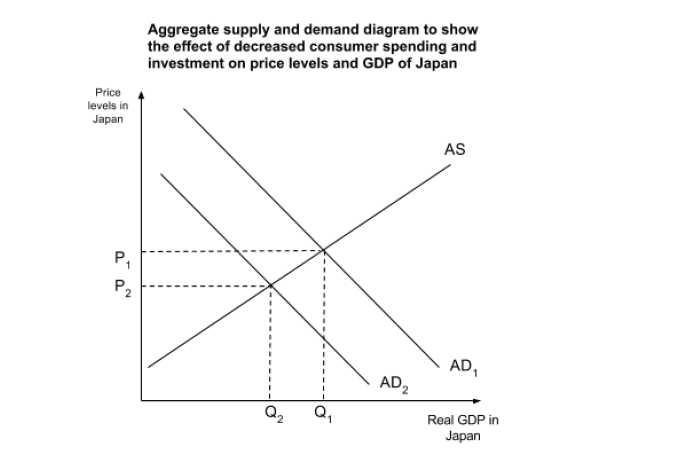

This is problematic because the aggregate demand (AD) shown in the diagram to the right is the summation of consumption, investment, government expenditure, as well as net exports, and since the consumption of households has decreased, AD also decreases, which is shown by the shift from AD1 to AD2. Now, because AD has shifted, the point of intersection with the aggregate supply curve has decreased both price levels from P1 to P2 and real GDP from Q1 to Q2. This indicates a decrease in the CPI or deflation, which can lead to a decrease in the real GDP.

This is problematic because the aggregate demand (AD) shown in the diagram to the right is the summation of consumption, investment, government expenditure, as well as net exports, and since the consumption of households has decreased, AD also decreases, which is shown by the shift from AD1 to AD2. Now, because AD has shifted, the point of intersection with the aggregate supply curve has decreased both price levels from P1 to P2 and real GDP from Q1 to Q2. This indicates a decrease in the CPI or deflation, which can lead to a decrease in the real GDP.

Deflation is problematic for a country trying to promote growth. While it might be thought that lower prices will increase consumer spending, the people in Japan, in anticipation of the deflation, choose to delay spending, especially on durable goods such as cars and washing machines, until they can get their goods at even cheaper prices. They are choosing future satisfaction over present satisfaction. This in turn decreases consumer spending, which then causes a further decrease in price levels and GDP.

Although consumers may enjoy the lower prices of the goods that they purchase, this is not the case for the firms that produce these goods. This is because while the final price of the product is lower, the production process (the costs of the raw materials and other inputs) was not available at the lower price levels, which means that relative to the final price, the product is more expensive to produce, which also means that the expected return will not have been met, decreasing profits. This may lower investment options for firms, and because investment is a factor of AD as stated, it will also shift the AD curve from AD1 to AD2, thereby decreasing the real GDP further.

What has been happening to wages? According to the article, Japan’s labor market is tight, meaning that the economy is close to achieving full employment. When the economy is close to full employment, the unemployed portion of the labor force is small, and available workers are more scarce. Suppose, in the diagram on the left, the demand for labour is at DL1. If the wage is at r 1, there is excess demand between Qs and Qd, which gives workers more power, and so there should be an upwards pressure on wages to r 2.

What has been happening to wages? According to the article, Japan’s labor market is tight, meaning that the economy is close to achieving full employment. When the economy is close to full employment, the unemployed portion of the labor force is small, and available workers are more scarce. Suppose, in the diagram on the left, the demand for labour is at DL1. If the wage is at r 1, there is excess demand between Qs and Qd, which gives workers more power, and so there should be an upwards pressure on wages to r 2.

However, in Japan, the wages seem to be stagnant and are not rising. What has happened? This again relates to deflation because as stated previously, “Slow wage growth is weighing on consumer spending”. The decrease in disposable incomes makes consumers less likely to spend more money. This, as shown in the first diagram, shifts AD left, and results in deflation which stunts economic growth.

Another alternative is that labour is making the choice not to demand higher wages, because they are more concerned with job security and the future than the present.

The government, through the BOJ, has made the choice to have an ultra-loose (expansionary) monetary policy, which means that interest rates are very low and the money supply is being increased. The aim is to shift AD right with more investment (the cost of borrowing is less) and consumption, because consumers will save less. Also, the yen will depreciate (weaken) making exports cheaper.

However, there are risks or large opportunity costs to this policy. Import costs will be much higher and it could lead to hyperinflation in the future. Savers are penalized by the low interest rates.

Japanese consumers, labour, firms and the government are all making choices that have an impact on their economy and on their well-being. But the outcome of those choices is not certain, while there has been some minor success that has been made in this front, the economy is still fragile.

Internal assessment criteria—SL and HL

Use the official IB economics IA criteria when assessing this work, available at: IA criteria

Portfolio (SL/HL)

Criterion A: Diagrams

Level descriptor

The two different diagrams provided are relevant and contain a suitable title and are correctly labeled. The explanations are generally good, but the Labor Force and DL2 curves require more explanation in diagram two. (2/3)

Criterion B: Terminology

Level descriptor

The appropriate macroeconomic terminology is used correctly throughout. (2/2)

Criterion C: Application and analysis

Level descriptor

The commentary uses an AD/AS diagram to analyse the article and this was applied effectively. The commentary also included a suitable discussion on expansionary monetary policies. (3/3)

Criterion D: Key concept

Level descriptor

The key concept of choice was used appropriately throughout the commentary. The way that choice is related to opportunity cost was stated explicitly. (3/3)

Criteria E: Evaluation

Level descriptor

Judgments were provied with appropriate reasoning, but the expansionary monetary policies required a fuller evaluation. (2/3)

General comments

The candidate picked a suitable article, selected an appropriate command term and produced a very good overall commentary. The overall score for this commentary was 12/14.